All Categories

Featured

Table of Contents

If you take a distribution against your account before the age of 59, you'll also need to pay a 10% charge. The IRS has imposed the MEC rule as a method to avoid people from skirting tax obligations. Unlimited banking only works if the cash money worth of your life insurance coverage plan stays tax-deferred, so make certain you don't transform your plan into an MEC.

Once a cash money worth insurance account categorizes as an MEC, there's no chance to reverse it back to tax-deferred status. Boundless banking is a feasible idea that supplies a range of benefits. Right here are a few of the pros of this one-of-a-kind, personal financing banking system. A non-correlated possession is any type of property not tied to the securities market.

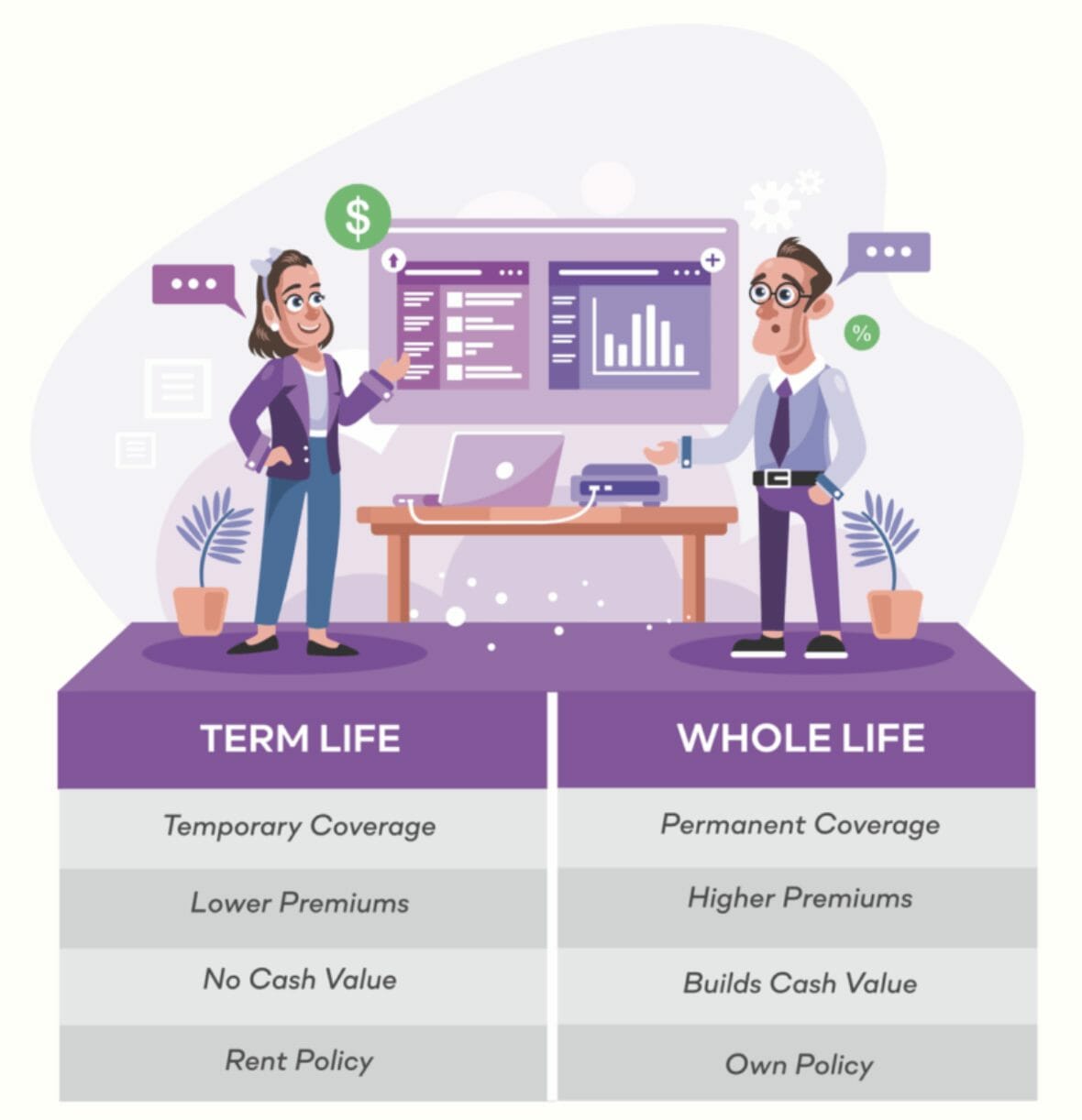

You can gain the benefits of unlimited financial with a variable global life insurance coverage policy or an indexed universal life insurance policy. Considering that these kinds of policies connect to the supply market, these are not non-correlated possessions. For your plan's money value to be a non-correlated asset, you will need either whole life insurance policy or universal life insurance policy.

Prior to choosing a plan, discover out if your life insurance business is a mutual firm or not, as only common firms pay returns. You won't have to dip right into your financial savings account or search for lenders with low-interest prices.

How can Tax-free Income With Infinite Banking reduce my reliance on banks?

By taking a lending from you as opposed to a conventional lender, the debtor can save countless dollars in interest over the life of the finance. (Simply be sure to charge them the very same rate of passion that you need to pay back to yourself. Otherwise, you'll take a financial hit).

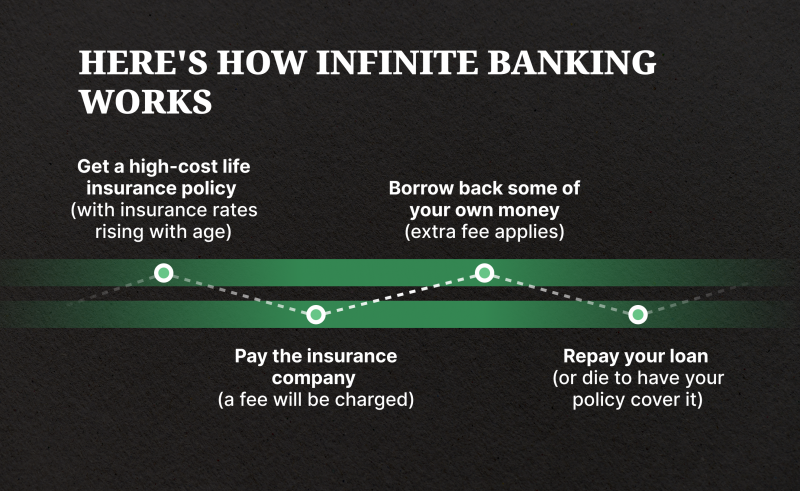

It's just one more way to delay paying taxes on a section of your earnings and create another safety and security web for on your own and your household. There are some drawbacks to this banking approach. Since of the MEC legislation, you can not overfund your insurance plan excessive or too swiftly. It can take years, if not years, to build a high cash worth in your life insurance policy plan.

A life insurance policy plan ties to your wellness and life span. Consequently, many insurance providers need a wellness examination or medical testing before the underwriting procedure can start. Depending on your medical background and pre-existing problems, you may not receive a permanent life insurance policy whatsoever. And if you don't certify, limitless financial the R

How can Private Banking Strategies reduce my reliance on banks?

Tired of depending on typical loan providers and big financial institutions? Fed up with paying high-interest prices when you require to get a lending? With boundless banking, you can become your very own lender, borrow from yourself, and include cash worth to a long-term life insurance policy policy that grows tax-free. Unlimited financial can be a peace-of-mind remedy for doctors, yet it's one of several approaches that you can utilize.

When you initially listen to about the Infinite Banking Concept (IBC), your very first reaction could be: This sounds too great to be true - Policy loans. The trouble with the Infinite Banking Concept is not the principle but those individuals offering an adverse critique of Infinite Banking as a concept.

So as IBC Authorized Practitioners via the Nelson Nash Institute, we believed we would address some of the top questions individuals look for online when finding out and recognizing whatever to do with the Infinite Financial Concept. So, what is Infinite Financial? Infinite Financial was developed by Nelson Nash in 2000 and fully discussed with the publication of his book Becoming Your Own Lender: Unlock the Infinite Financial Idea.

What resources do I need to succeed with Policy Loan Strategy?

You believe you are coming out economically in advance due to the fact that you pay no rate of interest, however you are not. When you conserve money for something, it generally means compromising something else and reducing on your way of living in other locations. You can repeat this procedure, however you are simply "reducing your means to riches." Are you satisfied living with such a reductionist or shortage state of mind? With saving and paying money, you might not pay rate of interest, yet you are utilizing your cash once; when you spend it, it's gone forever, and you surrender on the possibility to earn lifetime compound interest on that particular cash.

Billionaires such as Walt Disney, the Rockefeller household and Jim Pattison have actually leveraged the residential or commercial properties of entire life insurance coverage that goes back 174 years. Even banks use entire life insurance policy for the very same functions. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Income Agency (CRA) even acknowledges the value of participating whole life insurance policy as a special asset class used to create long-lasting equity safely and predictably and supply tax obligation benefits outside the scope of conventional financial investments.

What happens if I stop using Infinite Banking Wealth Strategy?

It permits you to produce riches by satisfying the banking feature in your very own life and the ability to self-finance significant way of living purchases and costs without disrupting the compound rate of interest. One of the simplest means to think of an IBC-type taking part whole life insurance coverage plan is it is comparable to paying a mortgage on a home.

When you borrow from your taking part entire life insurance plan, the money worth proceeds to grow undisturbed as if you never borrowed from it in the very first area. This is because you are using the money value and death advantage as collateral for a car loan from the life insurance coverage company or as collateral from a third-party lending institution (understood as collateral loaning).

That's why it's vital to collaborate with a Licensed Life Insurance policy Broker accredited in Infinite Banking that frameworks your getting involved entire life insurance coverage policy properly so you can stay clear of negative tax obligation ramifications. Infinite Banking as a monetary technique is not for every person. Right here are a few of the pros and cons of Infinite Financial you need to seriously take into consideration in determining whether to move on.

Our preferred insurance provider, Equitable Life of Canada, a common life insurance business, concentrates on participating entire life insurance policy policies specific to Infinite Banking. In a common life insurance policy firm, insurance holders are thought about firm co-owners and receive a share of the divisible excess generated yearly with rewards. We have a variety of carriers to select from, such as Canada Life, Manulife and Sunlight Lifedepending on the demands of our customers.

How do I track my growth with Financial Leverage With Infinite Banking?

Please additionally download our 5 Top Concerns to Ask A Boundless Banking Agent Prior To You Hire Them. For more details concerning Infinite Banking browse through: Disclaimer: The material offered in this e-newsletter is for informational and/or instructional purposes just. The info, point of views and/or views revealed in this e-newsletter are those of the authors and not necessarily those of the representative.

{kind=link}

Latest Posts

Being Your Own Bank

How To Train Yourself To Financial Freedom In 5 Steps

Non Direct Recognition Life Insurance